According to a recent CB insights research report, global Venture capital funded deals topped $39 billion in 2018 – a more than 100% increase over the previous year spanning 1707 deals. Fintechs are reinforcing themselves as a global phenomenon with regional hubs emerging around the globe outside the major markets of U.S, U.K & China. Looking past the euphoria of 2018, as these Fintechs begin to mature we are seeing some powerful new trends emerge where the existing ecosystem is being reshaped into something which serves the needs of the new tech-conscious consumer. The products & services are being catered to the needs of the growing segment of Millennials & Generation Zers. The report provides some great insights into how the Fintechs are transforming the financial landscape. Let’s review some of the main points.

➽ Fintechs have gotten aggressive in their approach of increasing their global footprint with mergers, acquisitions & partnerships – specially the European unicorns of Monzo, Revolut, and N26 which have established operational plans for the U.S in 2019. Digital banks have blossomed under the friendly regulation environment in Europe with GDPR & PSD2 guiding the way.

➽ The above mentioned M&A and partnerships have led the Fintechs to broaden the scope of their services beyond their initial niches. Below is the list of some of the Fintech startups which started off with a promising use case & ended up expanding into other lines of services.

Revolut (digital wallet) → Crypto trading, Brokerage services & Bank accounts

Wealthfront (robo-advisor) → College savings plan, Real estate investment, smart lending

Acorns (micro investing) → Wealth management, Bank accounts

Robinhood (brokerage) → Crypto trading, Margin investing, Bank accounts

MoneyLion (personal finance) → Wealth management, Smart lending, Bank accounts

Coinbase (crypto trading) → Institutional investing, Index investing, Wealth management

➽ Apart from diversifying the services to other segments of the financial services. The Fintechs are leading a movement to replace the old guard of brick & mortar banks with digital-only banks by applying for charters & licenses with the regulators. In the U.S, Green dot & Cambr launched something called the Banking-as-a-service platforms which facilitate third-party Fintechs to provide digital bank services to their clients. While others like NU bank, Varo, Zopa, Xinja & Revolut have also applied for banking licenses in various jurisdictions. Revolut is the most active member of this list which has already gotten banking licenses from Europe & Lithuania & is now looking to spread its services Singapore & Japan.

➽ The initial confusion & friction between the regulators and the Fintechs has transitioned into a building of partnerships. This has also been made possible with the emergence of RegTech regimes. Global regulatory regimes have been shifting their focus to promoting innovation & lowering barriers, bringing new products & services for the tech-savvy customers and breaking the monopolies of the traditional banks. Not to mention the fact the creation of regulatory sandbox has resulted in the development of RegTech tools, which not only adhere to compliance guidelines while monitoring transactions of these Fintechs, but also work as an early warning system to spot irregularities, potential threats & fraudulent transactions in the digital payment universe. The real-time reporting of these problems to the FinTech companies means that the problems can be rectified in a timely & efficient manner. It is important to note, however, that with access to Open banking APIs the Fintechs will eventually need to have in-house regulatory teams who can work with the regulators.

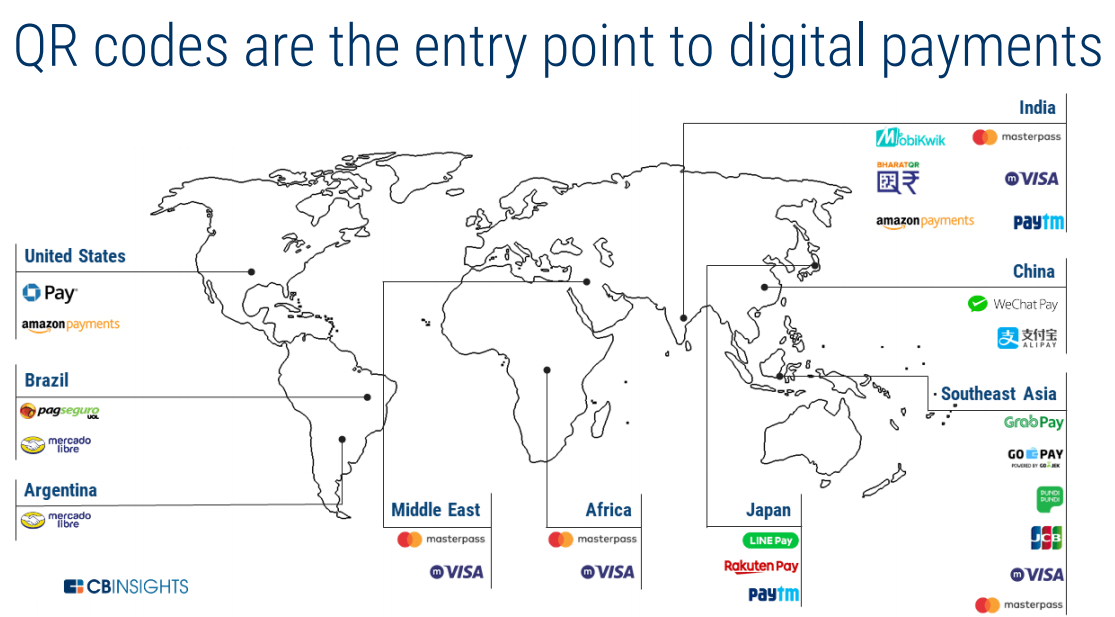

➽ 2018 was a bumper year for Fintech deals in South East Asia with record funding, up 143% YOY with the region attracting bigger investments from foreign investors. No doubt the region has become the hotbed of Fintech activity with companies like Alipay and WeChat leading China’s transition to a cashless economy. Popular Japanese messaging app Line is planning to build an ecosystem in the country based on the Alipay/WeChat Pay model. Meanwhile in South America, Argentinian e-Commerce player MercadoLibre is expanding its business QR code payments to facilitate the off payment channels which account for 30% of its total business volume. The Fintech operates a loan business & also plans to launch an investment fund for potential investors.

➽ Just like Blockchain has brought the concept of decentralization, Fintechs are creating New & Alternative models by democratizing the field of investing. This has been achieved in three waves:

- The first wave has lowered the barriers for investors with the help of technology to bring inclusiveness to those who were unable to access the markets beforehand due to regulatory, monetary or knowledge hurdles.

- Access to new asset classes is being made possible. A Prime example in this regards is direct Crypto trading, Securitized tokens, Digital asset indexes, Futures & derivatives etc.

- And then we have startups that are creating new investment models via the creation of Next-Gen investing platforms that can access the existing asset classes. These alternative investment apps will continue to gain traction with the tech-savvy segment of Millennials & Generation Z. Following are some of the prominent examples

Brokerages – Coinbase, Robinhood, EToro

Platforms – PeerStreet, roofstock, FUNDRISE

Marketplaces – EQUITISE, crowdcube

➽ And finally we are seeing the Rise of impact Fintechs. With global sustainability goals on top of the mind for policymakers, technology companies are taking on the challenges of ESG (environment, sustainability, and corporate governance) head-on. They are doing this by tapping into ESG & impact investing space which has seen an increased interest from both the economists & investors alike. The collective awareness to create social good apart from achieving personal financial goals is expanding this new segment of the market. With the demographic shift taking place the Fintech startups are creating Next-Gen wealth management platforms which not only serve the investment needs, but also align with the values of investors of which ESG is an integral part. The report suggests that the Impact Fintechs are making a mark in the ecosystem in two layers where the first layer is establishing green data credibility for the Financial services companies, while the second layer is establishing trust & credibility with the Next-Gen investors.

First Wave: Ethic (Advisory), CLARITY AI (Investing), SIGMA RATINGS (Credit Risk), Measurabl (Real Estate), TRU VALUE LABS (Data Integrity)

Second Wave: NEWDAY & Aspiration (Banking), Motif, Swell & OpenInvest (Investing), CNote (Lending)

Many traditional banks have been trying to play a catch up game with the upcoming Fintech wave. Be it Acquisitions, collaborations, digital banks or building Fintechs from scratch – the incumbents are trying everything to boost their digital capabilities. The challenger banks on the other hand have the technology, innovation spirit & an increasing global footprint on their side. It is pretty evident that Personal Finances, Banking & Investments are about to change in a fundamental way.

Email?| Twitter? | LinkedIn?| StockTwits? | Telegram?